Presented by Mark Gallagher

Coronavirus outbreak leads to mixed results for markets

January was a mixed month for markets, with concerns about the spread of the Wuhan coronavirus having a negative effect at month-end. Despite spending most of the month in positive territory, both the S&P 500 and the Dow Jones Industrial Average declined. The former fell 0.04 percent while the latter dropped 0.89 percent. The Nasdaq Composite also saw some late-month volatility, but previous gains were strong enough to leave the index up 2.03 percent for the month.

Despite the rocky ending to the month, fundamentals may be showing signs of improvement. Per Bloomberg Intelligence, as of January 31, the blended year-over-year earnings growth estimate for the S&P 500 in the fourth quarter is –0.3 percent. If this estimate holds, it would mark four straight quarters with earnings declines. The situation has been improving, however, and analysts are currently forecasting a return to growth in the first quarter of 2020. Fundamentals drive market returns, so earnings growth this quarter would create a tailwind for future returns. From a technical perspective, all three major U.S. indices remained well above their respective 200-day moving averages.

International markets had a tough start to the year, facing more volatility than their U.S. counterparts. The MSCI EAFE Index fell by 2.09 percent in January, with much of the decline coming in the final week of the month. The MSCI Emerging Markets Index faced pressure as well, falling 4.66 percent. Concerns about the coronavirus and the effect it could have on China’s growth were the primary causes. Both indices remained above their 200-day moving averages, though, indicating continued investor support.

The broad fixed income market, on the other hand, had a very strong start to the year, as the general risk-off sentiment drove investors into safe-haven assets. Long-term U.S. Treasury yields fell sharply in January. The 10-year yield declined from 1.88 percent at the start of the month to 1.51 percent at month-end. This brought yields on the long end of the curve back down to October lows and drove the Bloomberg Barclays U.S. Aggregate Bond Index to a gain of 1.92 percent.

Although investment-grade fixed income started the year off well, the same can’t be said for high-yield bonds. This portion of the fixed income market is typically not driven much by movements in interest rates; rather, it’s more correlated with equities, due to the speculative nature of high-yield bonds. High-yield spreads increased notably during the month, as investors demanded greater yield to compensate for the additional credit risk. The Bloomberg Barclays U.S. Corporate High Yield Index inched up by 0.03 percent.

Shifting geopolitical risks affect markets

January provided a prime example of why it is important to expect the unexpected and construct portfolios that can withstand short-term market volatility. Throughout the month, several geopolitical risks grabbed headlines and rocked markets.

The most significant was the discovery and spread of the coronavirus, which was declared a public health emergency by the World Health Organization at the end of January. Governments around the world have taken swift action to work toward halting the spread of the disease. Still, it has been the major driver of global market volatility.

Here in the U.S., the spread of the virus appears to be contained for now, so the effect on public health has been minimal. The potential economic impact is not yet clear, however. So far, travel and technology companies have been hit the hardest. But as we saw with the market sell-off at the end of the month, investors were also spooked by the continued spread of the disease and general uncertainty created by the situation. Ultimately, we can’t predict what the final economic cost and public health implications will be, so we can expect to see more volatility in line with the headlines.

Another major news story during the month was the escalation of military tensions between the U.S. and Iran. Notably, a U.S. strike killed an Iranian general in Iraq. It was followed by the retaliatory strike from Iran on two Iraqi airbases that were housing American military personnel. This unexpected development captured global attention due to the potential for further escalation in the war-torn region. Although this story was in the headlines for more than a week, its effect on financial markets was short-lived.

Both of these events showed how unexpected risks can grab investors’ attention and lead to market gyrations. As we saw with the Iran situation, though, once more clarity becomes available, markets can recover swiftly from these short-term jolts. Therefore, building a portfolio that can withstand the occasional bout of volatility should be an important goal for any investor.

Economic data improves

Despite the news-driven market turmoil we saw at month-end, the economic data releases in January continued to show improving fundamentals in the U.S. After staying rangebound for much of the fourth quarter, both major surveys of consumer confidence climbed by more than expected in January. A strong jobs market and increased optimism about future equity market returns drove much of this better-than-expected result. High consumer confidence often leads to additional consumer spending. So, seeing both confidence measures increase bodes well for first-quarter growth.

Consumer spending data was healthy, with the most recent retail sales report showing 0.3 percent growth in December. This brought year-over-year growth up to 5.8 percent, the highest it’s been since August 2018. Headline sales figures were held back by slow auto sales, though. Excluding cars, retail sales increased by a strong 0.7 percent in December, the best monthly result since July. Even though these retail sales results were strong, it was the housing sector that truly impressed.

Housing continues to be a bright spot in the economic expansion. Low mortgage rates and high consumer confidence have driven prospective buyers into the market. Existing home sales increased by more than expected during the month, reaching the highest level since February 2018. Even this strong result was likely held back due to lack of supply; existing homes available for sale have declined for seven straight months and are down 8.5 percent year-over-year. Declining supply is a headwind for potential home buyers, but it has been a boon for builders, who ramped up construction at the end of 2019.

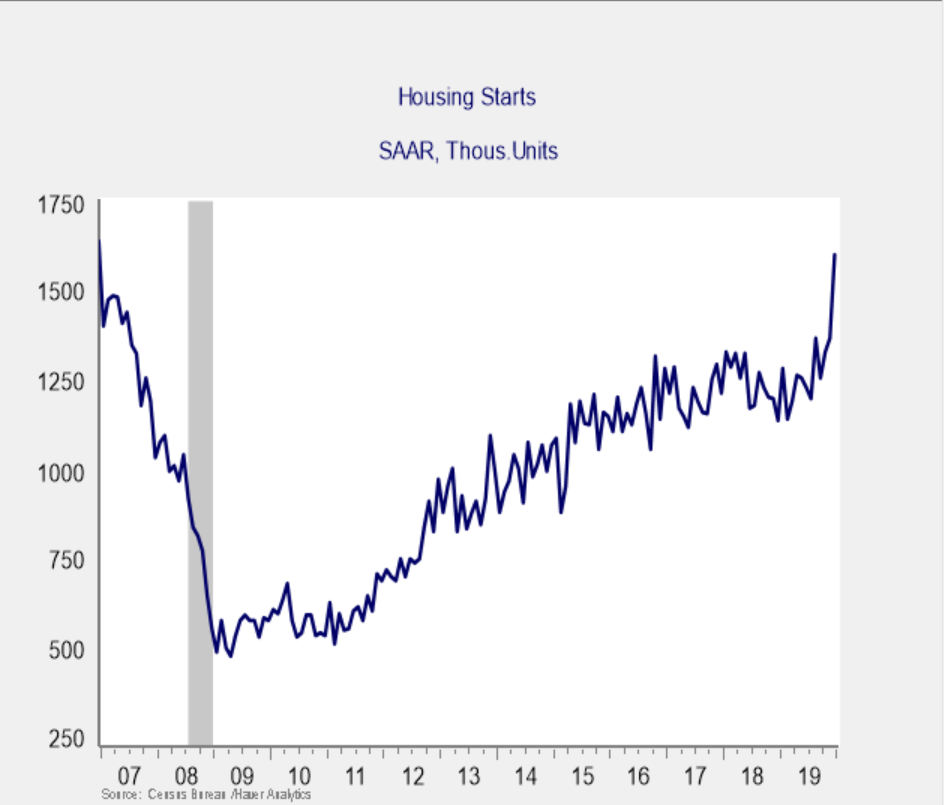

As you can see in Figure 1, housing starts grew dramatically at year-end, reaching post-recession highs. Home builder confidence remains near 20-year highs, driven by buyer foot traffic at levels last seen in 1998. We’ve already begun to feel the positive effects from this building spree on the economy. Residential investment grew at the fastest rate in two years in the fourth quarter, and it was a positive contributor to fourth-quarter gross domestic product growth. The housing sector has an outsize effect on the economy due to the associated knock-on purchases that come with buying a house. So, the rebound we saw at the end of 2019 is very welcome, and we appear to be poised for continued growth in the new year.

Figure 1. Housing Starts 2007–Present

Economy continues to grow, but risks remain

January showed how important it is to be aware that risks to financial markets can strike suddenly and without warning. The volatility we experienced at month-end was caused in large part by fear of the unknown, which can rock markets at any time.

From an economic perspective, the strong consumer surveys point to future spending growth. As long as consumers remain willing and able to spend, the economic expansion will likely continue, given the importance of the American consumer to overall economic health.

Remember, there is always the potential for suddenly emerging risks to affect markets, even when the economic environment is positive. That’s why a well-diversified portfolio that matches investor goals and time horizons remains the best path forward.

All information according to Bloomberg, unless stated otherwise.

Disclosure: Certain sections of this commentary contain forward-looking statements based on our reasonable expectations, estimates, projections, and assumptions. Forward-looking statements are not guarantees of future performance and involve certain risks and uncertainties, which are difficult to predict. Past performance is not indicative of future results. Diversification does not assure a profit or protect against loss in declining markets. All indices are unmanaged and investors cannot invest directly into an index. The Dow Jones Industrial Average is a price-weighted average of 30 actively traded blue-chip stocks. The S&P 500 Index is a broad-based measurement of changes in stock market conditions based on the average performance of 500 widely held common stocks. The Nasdaq Composite Index measures the performance of all issues listed in the Nasdaq Stock Market, except for rights, warrants, units, and convertible debentures. The MSCI EAFE Index is a float-adjusted market capitalization index designed to measure developed market equity performance, excluding the U.S. and Canada. The MSCI Emerging Markets Index is a market capitalization-weighted index composed of companies representative of the market structure of 26 emerging market countries in Europe, Latin America, and the Pacific Basin. It excludes closed markets and those shares in otherwise free markets that are not purchasable by foreigners. The Bloomberg Barclays Aggregate Bond Index is an unmanaged market value-weighted index representing securities that are SEC-registered, taxable, and dollar-denominated. It covers the U.S. investment-grade fixed-rate bond market, with index components for a combination of the Bloomberg Barclays government and corporate securities, mortgage-backed pass-through securities, and asset-backed securities. The Bloomberg Barclays U.S. Corporate High Yield Index covers the USD-denominated, non-investment-grade, fixed-rate, taxable corporate bond market. Securities are classified as high-yield if the middle rating of Moody’s, Fitch, and S&P is Ba1/BB+/BB+ or below.

Mark Gallagher is a financial advisor located at Gallagher Financial Services at 2586 East 7th Ave. Suite #304, North Saint Paul, MN 55109. He offers securities and advisory services as an Investment Adviser Representative of Commonwealth Financial Network®, Member FINRA/SIPC, a Registered Investment Adviser. He can be reached at 651-774-8759 or at mark@markgallagher.com.

Authored by Brad McMillan, CFA®, CAIA, MAI, managing principal, chief investment officer, and Sam Millette, senior investment research analyst, at Commonwealth Financial Network®.

© 2020 Commonwealth Financial Network®